Continuing last week’s article about whether high-income products rally make your life easier, we now look at two other types of high-income products: split-shares and covered-call ETFs.

Split-share corporations

Specialized investment corporations are created primarily to provide investors with a choice: a regular income stream or potential for capital appreciation. They do so by splitting their shares into two classes.

A split-share corporation is created by purchasing a diversified portfolio of common shares of other corporations, often blue-chip stocks. Then, the corporation issues shares:

Preferred Shares: usually offer regular dividends, have a set redemption value, and take precedence over other shares if the company is dissolved.

Preferred Shares: usually offer regular dividends, have a set redemption value, and take precedence over other shares if the company is dissolved.- Capital Shares (or Class A): are more volatile but provide potential capital appreciation. They receive the residual value after preferred shareholders are paid in full. They can show high returns if the portfolio appreciates, and large losses when the reverse happens.

Using the dividends of the underlying portfolio, split-share corporations pay the preferred shareholders first. They reinvest excess dividends into the portfolio or distribute them to capital shareholders.

Split-share corporations usually have a maturity date, when their sell their assets and pay the proceeds to shareholders. Again, preferred shareholders are paid first, up to their original investment plus accrued dividends. Remaining funds go to capital shareholders.

Create a long-lasting retirement income with our Dividend Income for Life Guide. Download it free!

Advantages and risks

Advantages of split share corporations include the choice between a more stable income or potential capital appreciation, tax advantages for some investors due to how they distribute the income, and potential for high income, as long as the company pays.

Unfortunately, they come with many risks. Not immune to market fluctuations, both preferred and capital shares can suffer if the portfolio’s stocks drop, with capital shares most vulnerable.

With an under-performing portfolio, many shareholders could redeem their shares, forcing the company to sell assets at an unfavorable time; capital shareholders might not recover their full investment upon the corporation’s maturity.

Split-share corporations often borrow to purchase assets, which amplifies both gains and losses based on asset performance vs. interest rates and heightens the volatility of capital shares. Poor-performing assets can also hinder loan repayment and affect the corporation’s credit rating.

Rising interest rates can devalue their portfolio just when fixed-income options become more attractive to investors.

Covered call 101

A call is an option granting the right to buy an asset at a set price within a specified period. Imagine DSR trading on the market with a stock price of $100. You buy an option to buy DSR stock at $105 in the next three months. If DSR stock surges to $120 during that time, you can buy the stock at $105, making an immediate profit. The owner of the shares who sells you the call option is writing a covered call.

Let’s say DSR trades at $100 with a dividend of $1 quarterly, a 4% yield. You hold shares bought at $100 per share. You write a call option on those shares, granting the buyer the right to buy 100 shares at $110. The buyer of pays you $200 for the option.

Let’s say DSR trades at $100 with a dividend of $1 quarterly, a 4% yield. You hold shares bought at $100 per share. You write a call option on those shares, granting the buyer the right to buy 100 shares at $110. The buyer of pays you $200 for the option.

If the stock price is stable or decreases, the buyer doesn’t exercise the option at $110, letting it expire. You keep your shares. You earned $200 from selling your option and another $100 in dividend (quarterly dividend of $1 X 100 shares). Selling the option generated additional income without any risk.

What if the stock price reaches $120? The buyer exercises the option; you must sell the shares at $110. You earn $200 from selling the option, $100 in dividend and $1,000 in profit (($110 – $100) X 100 shares), totaling $1,300.

Had you not sold the option, you’d show a paper profit of ($120 – $$100) X 100 shares = $2,000 of stock price appreciation, + $100 in dividend = $2,100. While you made money selling the option, you capped your total returns to the option price.

This is a popular strategy among income-seeking investors. So popular in fact, that there are several Covered Call ETFs offering juicy yields. But are they really worth the risk?

Create a long-lasting retirement income with our Dividend Income for Life Guide. Download it free!

Covered call ETFs

Writing covered calls can work well for individual investors, assuming they write judicious options; it’s a different story with manufactured covered call ETFs.

I suggest you watch this video about high yield covered call ETFs.

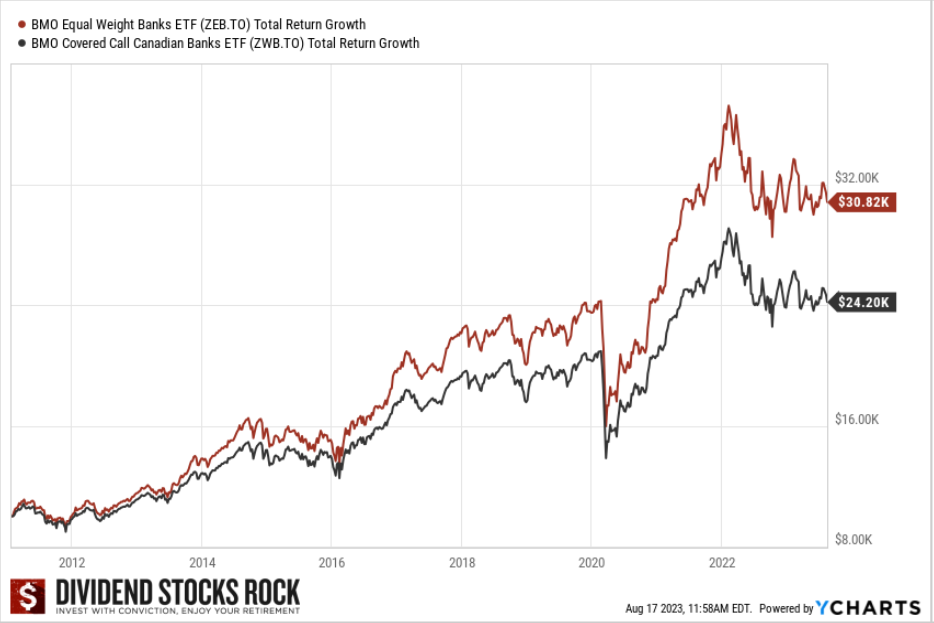

Let’s compare two ETFs, ZWB and ZEB, both manufactured by BMO, and both having a long history.

- ZWB is a covered call ETF on Canadian banks.

- ZEB is an equally weighted ETF on the big six Canadian banks.

This graph shows how much money investors leave on the table with ZWB for the sake of higher income. Imagine investing $10K in each product and reinvesting all dividends…

As of 08/17/2023, ZWB offers a 7.18% yield and ZEB about 4.41%.

If you really want the 7.18% yield, cash ZEB’s dividends and sell 2.77% extra of your investment monthly to equal that yield. Over time, you’ll have a lot more money in your pocket. You can withdraw more than 7.18% yield or withdraw 7.18% for longer. In both cases, the pure investment strategy generates better results.

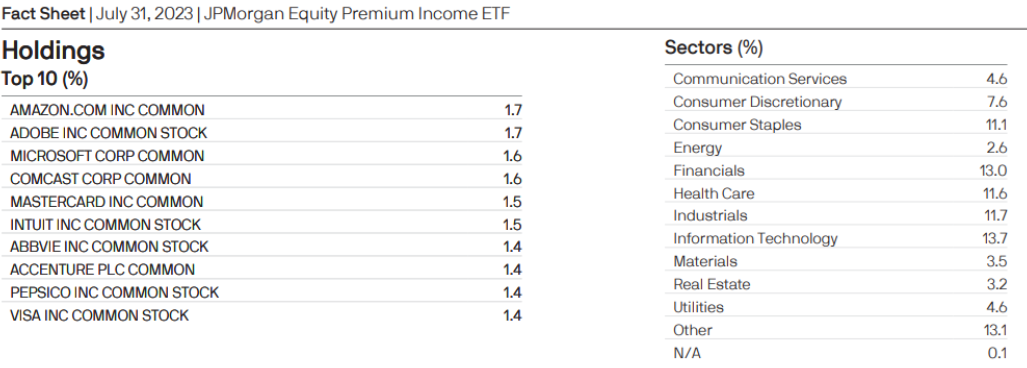

JPMorgan Equity Premium Income (JEPI)

Incredibly popular on the US market is JEPI with its yield >6%. This ETF uses options to generate a high yield from a well-diversified portfolio of 137 holdings.

Source: JPMorgan

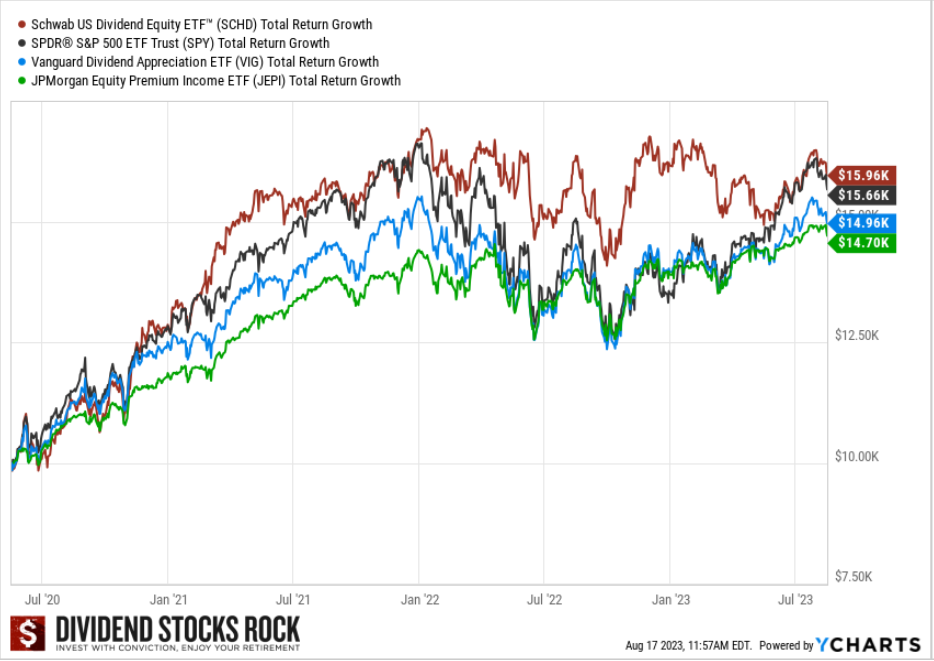

Sadly, we’re limited to a short history. Nonetheless, when comparing JEPI to classic investment strategies, i.e., dividend growth investing or index investing, we see similar results as in our earlier example.

The next graph shows the total return of a $10,000 investment, reinvesting dividends, of JEPI and these three investment vehicles:

| Investment vehicle | Description |

| Schwab US Dividend Equity (SCHD) | Dividend ETF focused on the Dow Jones U.S. Dividend 100 index |

| SPDR S&P 500 (SPY) | Classic index fund tracking the S&P 500 |

| Vanguard Dividend Appreciation ETF (VIG) | Dividend growth ETF |

Where’s the investment in JEPI after three years? At the bottom. As it was for the Canadian Bank ETF vs. Canadian Bank Covered Call ETFs, the income-focused product finishes dead last.

Conclusion

While covered call ETFs aren’t the worst products, they don’t provide added value compared to index or dividend growth investing. Focusing on high-income products often means leaving money on the table.

A classic investment strategy that generates a higher total return will serve you better. Then, you can sell a few shares and create your own retirement income.